What Does a Court Judgement Mean on My Credit File?

A court judgement on your credit report indicates that a court ruled against you. This typically happens due to a financial dispute between you and a creditor. As a result, the court may order a default judgement, requiring you to make a payment to the creditor or debt collector. Additionally, this judgement allows the creditor or debt collector to take enforcement action to compel you to pay the debt.

- A default judgment occurs as a result of the debt collection process. Consequently, your credit file will show the negative outcome of the court hearing.

- Moreover, the court's decision confirms that you owe the money.

- Furthermore, the court can impose legal costs on you.

- Also, It will also set deadlines for paying the judgment debt.

- Finally, a court judgment negatively impacts your credit score and credit report, affecting future credit applications.

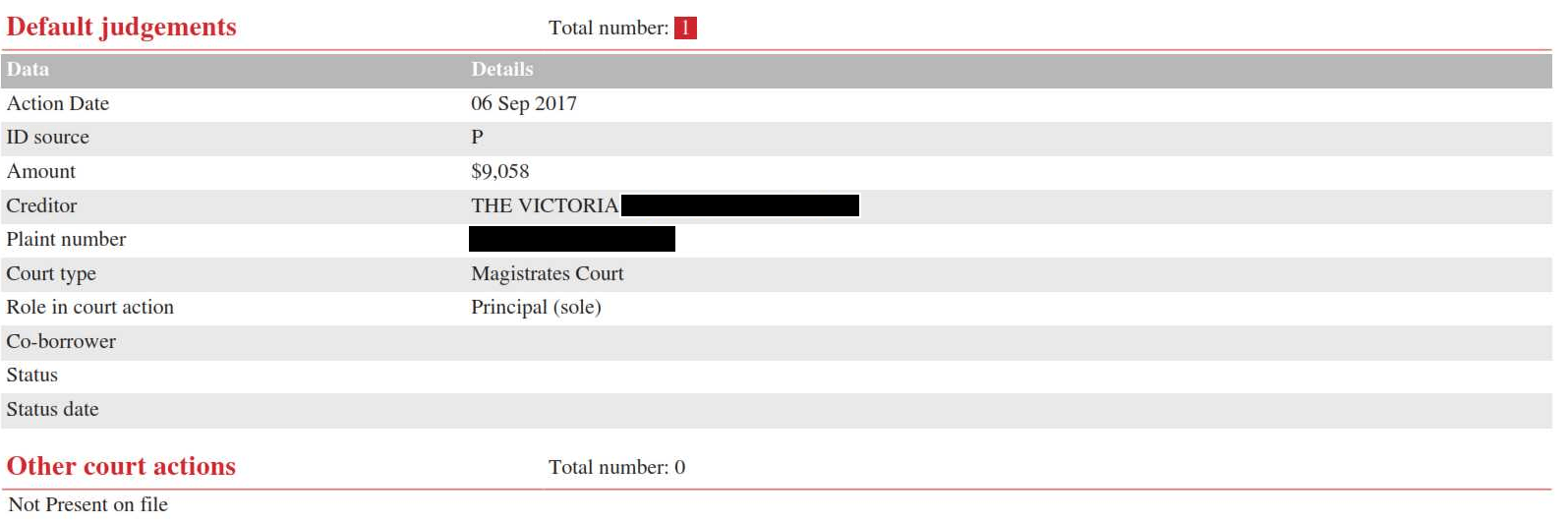

Court Judgment Information Listed on Your Credit File

Court outcomes on your credit report indicate similar information as a credit default. However, court results also record the court type and the plaint number (court reference). Court judgments provide the following details:

- Firstly, they include various creditor information such as the name of the creditor and the amount of debt.

- Secondly, they detail current and pending actions. As such, court information on your credit file can identify future escalation of credit issues.

- Therefore, it indicates that a creditor may seek further recovery, such as bankruptcy.

- Finally, a court judgment will remain on your credit file for five years if paid before that period, or seven years if not paid in full.

Typical Court Judgments We See:

- Firstly, the Australian Taxation Office may issue a tax debt judgment.

- Secondly, creditor judgments come from various creditors or debt collectors, such as GE, Lion Finance, and ACM Group.

- Additionally, businesses you owe money to can take you to court. If the court rules that you owe money, it will issue a judgment against you.

How Can the Court Force a Judgment Payment?

There are several ways a court judgment can force payment of monies. Indeed, once the sentence has been passed, the creditor can apply to the court for the following:

- Firstly, an instalment order, where you pay the debt in instalments.

- Secondly, a garnishee order, which allows the court to force payment by directly debiting your bank account. Additionally, the court can order a garnishee against your income. Furthermore, the ATO or other creditors can force a garnishee against future invoices by contacting your customers directly.

- Lastly, asset seizure and sale, where the court forces the repossession of fixed or movable assets for sale to repay your creditor.

I've Paid My Debt to the Creditor! Why Is My Court Judgment Listed as Unpaid?

Court judgments are outcomes of court proceedings. Therefore, the creditor doesn't update your credit file directly. The reason for this occurrence is two-fold:

- Initially, the court records the judgment outcome. Consequently, the creditor usually needs to attend the court to update the outcome.

- Secondly, when you pay a creditor, they are not the party who updates your credit file to "paid" status. Therefore, the creditor must notify the court. Then, the court notifies the credit reporting agency.

- Consequently, updating your credit file is not typically a creditor process. Therefore, you will need to contact the creditor and request that the court judgment be updated. Alternatively, you can obtain a receipt of payment with the correct payment date and provide it to the court yourself.

- Also, the courts may require a fee for updating the court record.

Notice of Discontinuance

How can you remove court judgments from your credit file? Firstly, the creditor needs to provide a letter of discontinuance. Consequently, you can obtain this discontinuance letter directly from the court.

However, not all creditors will sign a notice of discontinuance to remove the court judgement.

Each judgement ruling can have a different collection outcome. Hence, the verdict and collection can vary depending on the court, creditor, judge attending to your case, and your attendance.

If you have a pending or current court judgement, you should:

- Assess your risk of bankruptcy and loss of assets.

- Next, find out your available solutions to resolve the judgement debt.

- Finally, obtain legal or financial counselling.

Courts That Can Assign Financial Judgments

- Initially, the Magistrates' Court is used for most minor matters, such as traffic offenses.

- Secondly, the County Court handles more serious crimes and claims over $100,000.

- Finally, the Supreme Court deals with the most serious criminal cases, often requiring a judge and jury. Additionally, the Supreme Court addresses financial matters over $200,000.

Courts That Usually Don't Incur Financial Outcomes

- Children's court handles matters related to children. As such, we don't usually see financial outcomes from the Children's Court.

- Similarly, the Coroners Court investigates matters related to unexpected deaths or cases where a body cannot be found. However, we don't see financial or court judgment outcomes from this court either.

- The Neighbourhood Justice Centre, a Victorian court associated with the City of Yarra, is not used for monetary claims.

For more information, you can refer to the related article from Legal Aid Victoria: The Victorian courts and tribunals

Loan Saver Network Services

Loan Saver Network offers free and confidential debt consultation. Hence, we seek to resolve credit issues with a range of finance products. Additionally, we advise on other strategic solutions to minimize risk and improve your chances of success.

We recommend obtaining legal advice for any court matter. Consequently, you may use your solicitor or legal aid for advice. Furthermore, you may receive financial assistance from a financial counselor who can inform you of your rights regarding financial hardship.

Related Articles:

- Refinancing solutions when seeking a debt consolidation or bad credit home loan.

- Loans to pay a tax debt when the ATO has listed a court judgement.

Let's talk about a solution that suits you

1300 769 850

1300 769 850