How Credit Defaults Affect Your Loan Applications

When you apply for a loan, lenders will check your credit report for any credit defaults or issues. They do this to learn about your financial history or credit rating. A credit reporting body records credit history, and several agencies handle this process.

Credit defaults can greatly affect your borrowing options. Knowing how they impact your applications can help you manage your finances better.

What Lenders Look At

Lenders examine several aspects of defaults when assessing your application:

- Payment status: Paid vs unpaid defaults

- Quantity: Total number of defaults on your file

- Age: How recent the defaults are

- Resolution time: How quickly you settled after the default was listed

- Type: Whether they're consumer or commercial-related defaults.

- Credit Type: A credit reporting agency keeps track of different types of credit. This includes credit cards, personal loans, and car loans.

Each default stays on your credit report for five years, even after you've paid it off. While paid defaults look better than unpaid ones, they still affect your credit score.

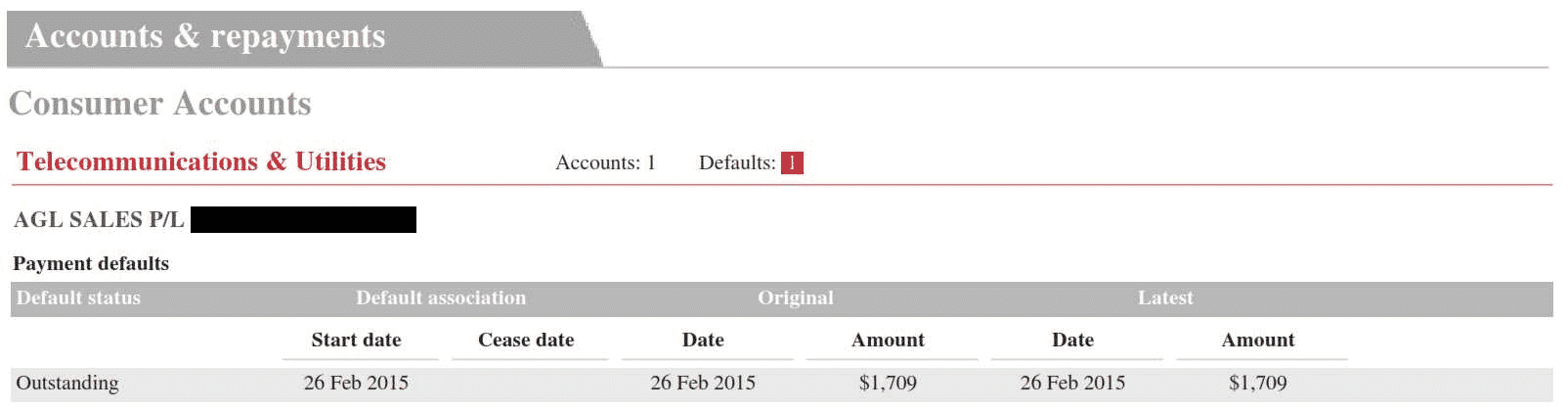

The credit report includes details and specific information related to the default. Therefore, lodgement date, default amount, plus the date of payment.

Defaults stay on the credit file for five years from lodgement. As such, the default in the table below will drop off the credit file 26/02/2020.

How Does a Credit Default Affect Borrowing Options

With defaults on your record, you'll typically face:

| Impact | What it means for you |

|---|---|

| Limited lender options | Fewer lenders willing to approve you |

| Higher interest rates | You'll pay more for borrowed money |

| Stricter requirements | Possibly larger deposits or additional security needed |

| Specialised products | You may need bad credit loan options |

Avoid Making Things Worse

Be careful about multiple applications! Each time you apply for credit, it's recorded on your file along with your repayment history. Applying for many loans when you have defaults can lower your credit score even more. This can create a negative cycle that makes getting approved even harder.

- Check your current credit score before applying anywhere.

- It’s a good idea to get professional advice. They can help you find lenders who might consider your situation.

Taking a strategic approach to loan applications when you have defaults gives you a much better chance of success.

Remember that different lenders have different rules. Some may approve your application, while others may decline it. This can happen even in the same situation, especially with mortgage arrears or refinancing needs.

FAQ's about Credit Defaults

Credit Default FAQs

Defaults can only be removed if they were listed in error. Credit repair requires valid reasons for removal include:

- The default was listed incorrectly

- You never received proper notice

- The debt wasn’t yours

- The amount listed was wrong

If there’s no error, you’ll need to wait out the five-year period. Paying the default won’t remove it, but it will update the status to “paid” which looks better to lenders.

Defaults have a specific timeframe on your credit report. A default will remain on a credit report for five years, even if you pay it off completely.

If you pay the default:

- The status changes to “paid” or “settled”

- It still stays on your report for the full five years

- It looks better to potential lenders than an unpaid default

The five-year period starts from the date the default was listed, not from when the debt occurred.

A default can have several consequences:

| Impact | What It Means For You |

|---|---|

| Lower credit score | Makes borrowing more difficult |

| Higher interest rates | More expensive loans if approved |

| Loan rejections | Banks may decline your applications |

| Utility connection issues | May need to pay deposits for services |

| Rental application problems | Landlords may reject your application |

These effects can last for years, so addressing defaults promptly is important.

Finding defaults on your credit report is straightforward:

- Request a free copy of your credit report from credit reporting agencies like Equifax

- Check your credit score for free through various online services

- Review the “defaults” section of your report carefully

- Look for any errors or unfamiliar entries

It’s smart to check your credit report annually, even if you don’t suspect any defaults.

A credit default is an overdue debt of $100 or more that hasn’t been paid by the agreed date. For a debt to be listed as a default:

- The debt must be at least 60 days overdue

- The creditor must have sent you notices requesting payment

- The creditor must have notified you that they intend to list a default

Defaults are serious matters that indicate you’ve failed to meet your payment obligations.

If you receive a default notice, don’t panic! Here are some steps to take:

A creditor default notice may or may not have listed a credit default on your credit file. However, check carefully.

- Read the notice carefully – Check all details including the amount and creditor

- Contact the creditor – Try to negotiate payment arrangements

- Seek financial advice – A financial counsellor can help with options

- Consider a payment plan – Work out what you can afford to pay

- Keep records – Document all communications with the creditor

Getting help early can prevent the default from being listed on your credit report.

1300 769 850

1300 769 850