Debt Consolidation Solutions

When They Work — and When They Don’t

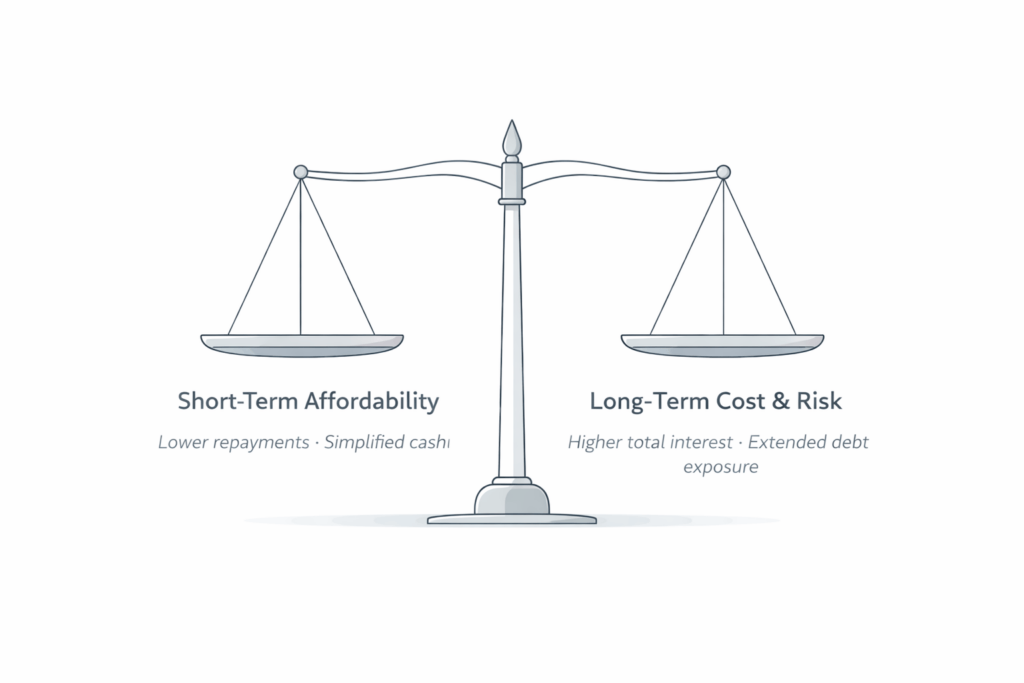

Debt consolidation is often presented as a simple way to reduce repayments and regain control of multiple debts. However, in practice, it is a strategic financial tool, not a universal solution. In many situations, debt consolidation can improve short-term affordability. In others, it can increase long-term risk and delay more appropriate action.

For this reason, debt consolidation should never be assessed in isolation. Instead, it must be considered alongside income stability, debt type, credit history, and longer-term financial objectives. This page explains when debt consolidation works, when it doesn’t, and how professionals assess suitability before recommending any loan structure.

What Debt Consolidation Is — & What It Is Not

Debt consolidation involves combining multiple existing debts into a single facility, with one repayment and one structure to manage. As a result, borrowers often experience simplified cash flow and improved repayment visibility.

However, debt consolidation does not eliminate debt, nor does it automatically fix the cause of financial stress. While it can restructure repayments, it does not remove underlying issues such as income volatility, structural overspending, or unresolved arrears.

Therefore, consolidation should be viewed as a management strategy, not a reset button.

Why People Consider Debt Consolidation

In many cases, ongoing debt pressure is not caused by a single loan but by deeper financial patterns and life events. Indeed, this is why understanding the real reasons debt becomes unmanageable is often more important than restructuring repayments alone.

Managing Multiple Repayments and Cash-Flow Pressure

When several debts operate simultaneously, repayment dates, interest rates, and minimum amounts can quickly become unmanageable. Consequently, cash flow becomes reactive rather than planned, increasing the likelihood of arrears.

Escalating Interest, Arrears, and Credit Stress

High-interest credit products, particularly unsecured facilities, can escalate rapidly when only minimum repayments are made. As a result, balances may increase even when regular payments continue. Over time, this often leads to credit stress, defaults, or collection activity.

When Debt Consolidation Can Be an Appropriate Strategy

While consolidating multiple debts may improve short-term affordability in some circumstances, determining suitability requires careful assessment. As a result, this is explored in detail in whether a debt consolidation loan is a good idea in your situation.

Situations Where Consolidation May Improve Short-Term Affordability

If income is stable and debts are manageable but poorly structured, consolidation may reduce repayment pressure. For example, replacing multiple high-interest debts with a lower-rate facility can improve monthly affordability while restoring predictability.

When Consolidation Can Prevent Further Credit Deterioration

In some cases, consolidation may help prevent arrears from escalating into defaults or legal action. By restructuring repayments before further damage occurs, borrowers may stabilise their position and protect their credit file from additional harm.

However, these outcomes depend entirely on suitability, structure, and timing.

When Debt Consolidation Is the Wrong Solution

Although widely promoted, debt consolidation is not appropriate in every situation. In fact, using consolidation incorrectly can worsen outcomes.

Where income is unstable or debts have already escalated into arrears, defaults, or legal arrangements, consolidation can increase long-term risk, making it critical to understand when a debt consolidation loan makes sense — and when it does not before proceeding.

Scenarios Where Consolidation Increases Long-Term Risk

Extending short-term debts into longer facilities can significantly increase total interest paid. While repayments may reduce initially, the overall cost of debt often rises. In addition, securing unsecured debt against long-term assets can increase exposure if circumstances change.

When Other Debt Solutions Are More Appropriate

If income is unstable, debts are already in default, or the underlying issue remains unresolved, consolidation may simply delay inevitable outcomes. In these situations, alternative strategies — such as negotiated arrangements, hardship options, or formal insolvency pathways — may provide a more sustainable resolution.

For this reason, professional assessment is critical before proceeding.

Key Risks and Trade-Offs to Understand Before Consolidating Debt

Before consolidating, it is essential to understand both the benefits and the risks.

Lower Repayments vs Higher Total Interest

While consolidation often lowers monthly repayments, it can also increase the total interest paid over time. Therefore, any short-term relief must be weighed against long-term cost.

Credit File Impacts and Future Borrowing Consequences

Consolidation may improve repayment consistency. However, it can also affect future borrowing capacity, particularly if higher-risk products or extended terms are involved. As a result, long-term objectives must be considered alongside immediate relief.

How Debt Consolidation Is Assessed by Professionals

A responsible consolidation assessment focuses on suitability, not approval.

Income Stability and Repayment Capacity

Professionals assess whether income can support the new structure sustainably, not just at the point of approval.

Nature and Status of the Debts Being Consolidated

The type, age, and status of debts matter. For example, debts in arrears, default, or legal escalation require different consideration than current accounts.

Exit Strategy and Long-Term Financial Objectives

Finally, consolidation must align with a clear exit strategy. Without one, borrowers risk remaining in long-term debt without resolution.

Professional assessments focus on suitability rather than approval, and a practical example of how this judgement is applied can be seen in a real-world debt consolidation case study.

Debt Consolidation Compared With Other Debt Solutions

Debt consolidation is only one option among several.

Informal Arrangements and Hardship Options

In some cases, negotiating directly with creditors or accessing hardship support may stabilise repayments without introducing new debt.

Part 9 Debt Agreements and Insolvency Pathways

Where debts are no longer serviceable, formal arrangements may provide a clearer resolution. While these options carry consequences, they may be more appropriate than extending unsustainable debt.

Formal debt arrangements also involve additional legal and credit considerations, which is why understanding how Part 9 debt agreements interact with consolidation requires specialist assessment. Independent guidance on formal debt agreements is also available through government insolvency authorities.

Choosing the Right Debt Strategy for Your Situation

Debt consolidation can be effective when used correctly, but it should never be the default response to financial stress. The right strategy depends on your income, debts, credit position, and long-term goals.

Decisions made to manage debt today can affect future borrowing options, making it important to understand how current debt arrangements may impact future home loan eligibility in certain circumstances.

Rather than focusing on speed or approval, the priority should be making the right decision in the right order.

If you are unsure whether debt consolidation is appropriate, the next step is a structured assessment — not an application.

Assess Whether Debt Consolidation Is Right for You

If you are unsure whether debt consolidation is appropriate, the next step is a structured assessment—not an application.

Alternatively, call 1300 796 850 if you would prefer to discuss your situation.

Debt Consolidation FAQ's

Debt Consolidation Pillar FAQs

No. Debt consolidation can be helpful in some situations, but it is not suitable for everyone. Outcomes depend on income stability, the nature of the debts, credit position, and long-term objectives. In some cases, alternative strategies may be more appropriate.

Yes. While consolidation can improve short-term affordability, it may also increase the total interest paid over time. This trade-off is why professional assessment is important before proceeding.

No. Consolidation restructures how debts are managed, but it does not resolve underlying issues such as income volatility, overspending, or unresolved arrears. These factors must be addressed separately.

Suitability is assessed by reviewing income stability, repayment capacity, the status of existing debts, credit history, and long-term financial goals. The focus is on sustainability, not approval.

Alternatives may include hardship arrangements, informal negotiations, or formal insolvency pathways, depending on the circumstances. Each option carries different consequences and should be assessed carefully.

1300 769 850

1300 769 850