Your credit score plays a big role in your financial life. Lenders check it before approving loans, credit cards, and even rental applications. A good score can get you better interest rates, while a low score can make borrowing harder.

Understanding how scores work helps you take control of your financial future. This guide will explain how scores are calculated, why they matter, and how you can improve yours.

What is a Credit Score?

A credit score is a number that shows how well you handle debt. Lenders use it to decide if they should approve your application. It also affects the interest rates and credit limits they offer.

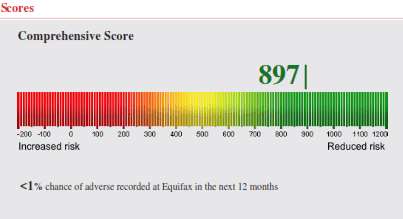

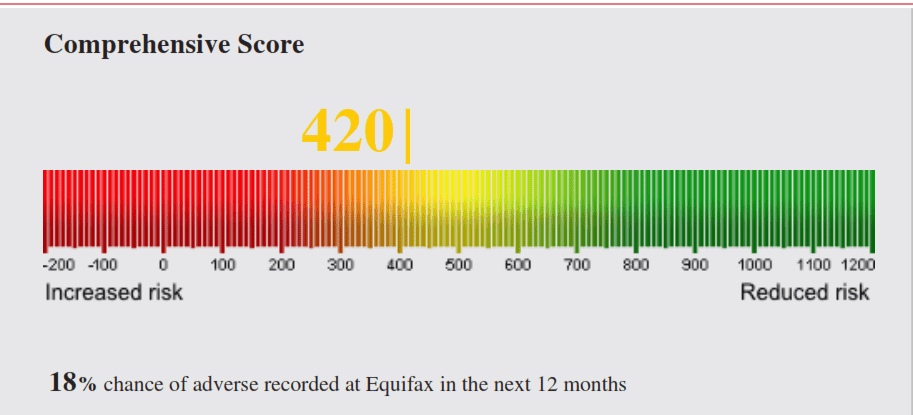

In Australia, scores range from 0 to 1,200. A higher score means less risk to lenders, which can lead to better borrowing terms.

Credit Score Ranges in Australia

- Excellent (833-1,200): Best rates and easiest loan approvals.

- Very Good (726-832): Lower interest rates and strong approval chances.

- Good (622-725): Most lenders will approve, but rates may be higher.

- Fair (510-621): Limited options and higher interest rates.

- Low (0-509): High risk; may struggle to get credit.

Source: Equifax Credit Score Guide

Negative Score Information: What You Need to Know

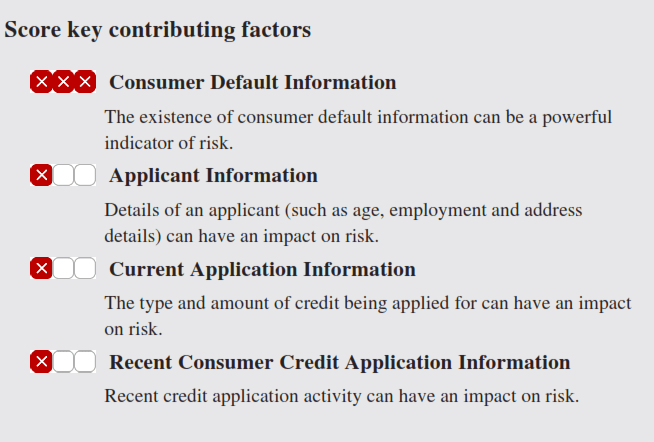

Your credit score is affected by negative information recorded on your credit file. One of the biggest changes in recent years is the inclusion of repayment history. Lenders can now see up to two years of repayment records for credit cards and other loans. If you miss a payment by more than 30 days, it will be marked on your file, which can lower your score. As such, prolonged arrears can significantly affect credit standing.

A credit default has an even bigger impact. Defaults signal serious repayment issues, making it harder to get approved for credit. In addition, court judgments, writs, and company liquidation records can damage your credit profile. If you are a company director involved in winding-up proceedings, this can also appear on your file.

The most severe impact comes from bankruptcy. Declaring bankruptcy may result in a period where no active credit score is available, with records remaining visible for several years. The same applies to other insolvency arrangements, such as Part 10 Personal Insolvency Agreements (PIA) and Part 9 Debt Agreements under the Bankruptcy Act. These actions remain on your credit file for several years, affecting your ability to borrow in the future.

Monitoring your credit file and keeping up with payments can help you avoid negative listings and protect your financial future.

Figure 1

Figure 2

Figure 3

wondering about a credit report

Competitive Interest Rates

Free Credit Report

How Do Credit Bureaus Calculate Scores?

Your score depends on several key factors:

👉 Payment History – Paying on time boosts your score, but late payments lower it.

👉 Credit Utilization – Using less than 30% of your available credit helps.

👉 Credit Age – Older credit accounts show stability and improve your score.

👉 New Credit Applications – Too many applications in a short time can hurt your score.

👉 Credit Mix – A mix of credit types (loans, credit cards) shows responsible borrowing.

Why Your Credit Score Matters

Your score affects loan approvals, interest rates, and financial opportunities. Here’s how:

💰 Loan Approvals: When lenders assess consolidation applications.

🏠 Interest Rates: A better score means lower interest rates, saving you money.

🚗 Insurance & Rentals: Some landlords and insurers check credit scores before approving applications.

Equifax One Score: A Smarter Credit Model

Equifax One Score is a new way to assess credit risk. It gives lenders a better view of your financial health by including:

✔️ Comprehensive Credit Reporting (CCR) – Two years of repayment history.

✔️ Buy Now, Pay Later (BNPL) Data – Tracks modern spending habits.

✔️ Geodemographic Data – Considers location-based financial trends.

This updated model helps lenders make better decisions while giving consumers more control over their credit.

Learn More: Equifax One Score

If you are unsure how your credit history may affect available options, an assessment can help clarify position, constraints, and next steps.

How to Improve Your Credit Score

Credit scores may improve over time when certain factors change. Common contributors lenders look at include:

✅ Pay Bills on Time – Set reminders or automate payments.

✅ Limit Credit Applications – Too many applications in a short period can lower your score.

✅ Keep Credit Card Balances Low – Use less than 30% of your credit limit.

✅ Check Your Credit Report – Look for errors and fix them.

✅ Use Different Credit Types – A mix of credit cards and loans shows responsible credit use.

Why You Should Monitor Your Credit Score

Credit monitoring helps you stay on top of changes in your report. It also protects you from fraud. Here’s why it’s useful:

🔔 Get alerts when your credit report changes.

🔍 Spot identity theft early.

📊 Understand how financial decisions impact your score.

Take Charge of Your Credit

Your credit score is one of your most important financial tools. By checking it regularly, making smart financial choices, and using credit monitoring, you can improve your score and open more financial opportunities.

💡 Need help managing your credit? Contact Loan Saver Network for expert advice on 1300 796 850.

1300 769 850

1300 769 850